Consumer debt hit a record high in the second quarter

Consumer debt hit a record high in the second quarter

www.consumeraffairs.com

Consumer debt hit a record high in the second quarter

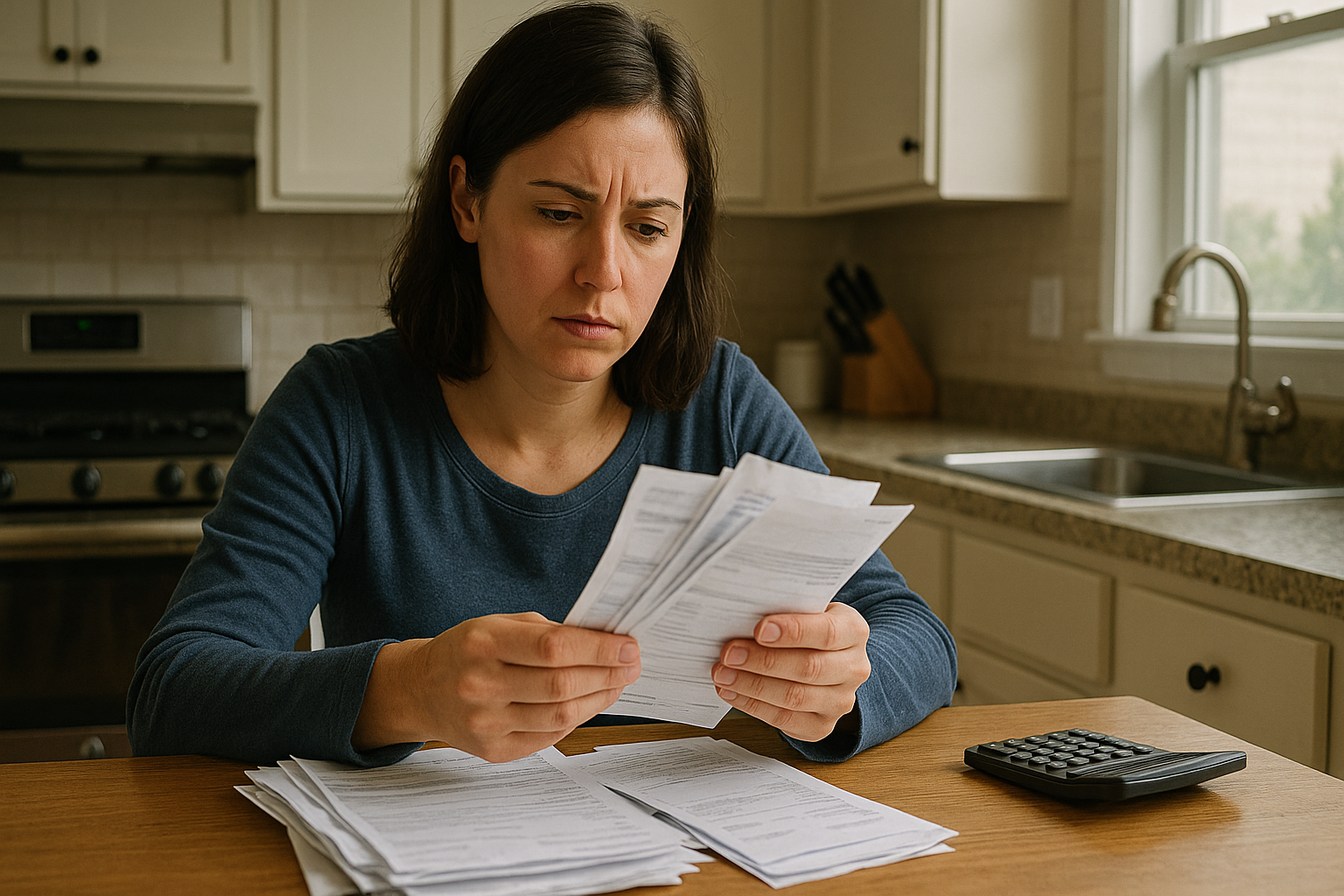

U.S. household debt increased by $185 billion in Q2 2025, reaching $18.39 trillion.

So when's the debt bubble going to burst? Because this obviously isn't sustainable

It's all according to plan, next the debt can be bought, and lead people into slavery.

I'm personally saving up to make use of that opportunity when it arises. IMO the future looks amazing!

/s

Why would it burst? Human history is filled to the brim with times where one a few lorded over the rest.

People got caught up in the left vs right and not the up vs down.

Tax wealth, not work.

Do you think it scales with population growth and current communication methods? Genuine question.

We have 8 billion interconnected humans on the planet now. Not just a few farmers and peasants. I feel these are different times.

History is repeating, yes. But I think it's a mistake for those few lords to assume everything will roll back a century or two. The people (those who dont want to be ignorant) are informed and well armed these days.

Edit: grammar and typo

Thats the neat part, it doesn't!

What does burst, instead, is the average net worth of Americans / Households.

We are at something like 10 to 15 % of Americans with a negative net worth right now, more debt than wealth.

So, welcome to the semi-formal birth of the debt slave social caste!

Ain't nobody working the farms no more, and indentured servitude is explicitly legal in the US as punishment for a crime.

If your crime is avoiding debt collectors long enough that they file a lawsuit against you, and you don't show up to court, well now you have an active arrest warrant.

And soon, probably also a non voluntary vacation to a semi-local farm.

Well, if we end up in runaway inflation - and that’s very possible, because the people running this place would have trouble assembling a Duplo set - we’ll all be able to pay off our debts for pennies on the dollar.

You are partially correct.

The problem is that you assume that during hyperinflation, you do not also have a massive rise in unemployment.

Historically speaking, this is a very noncredible assumption.

Also, even without that... you are still assuming symmetric inflation, broadly the same, everywhere.

That isn't guaranteed at all, this is another historicslly noncredible assumption, there's no fundamental reason that wages would not continue to increase by far less than every other daily cost of living.

So... sure, if you can survive that, remain employed, and your wages increase by more than the APR on your debt, oh right and dodge all the bank failures potentially wiping out your savings... uh sure ues then your plan may work.

Oh! Yeah, gotta also hope what is almost certainly your primary investment ... your house... does not collapse in value in real terms.

Uhm, roughly half the US is currently undergoing a massive housing market crash, so, again, not a great assumption.